For agencies and educational partners planning ahead, one question shapes every decision: are the destinations you recommend built on solid ground? In early 2026, two of the destinations at the heart of MLA’s programme portfolio — the United Kingdom and Ireland — answered that question with unusual clarity. Within the space of a few weeks, both governments reaffirmed international education as a national priority, and both did so while placing quality and sustainable recruitment at the centre of their plans.

For partners who send junior and teen students abroad each summer, this is more than policy news. It is a signal about where the market is heading, and it is worth reading closely.

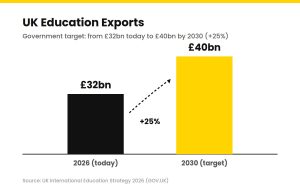

The UK Sets a £40 Billion Ambition

On 20 January 2026, the British government published its new International Education Strategy 2026, developed jointly by the Department for Education, the Foreign Office and the Department for Business and Trade. The headline is striking: the UK aims to grow its education exports to £40 billion a year by 2030, up from around £32 billion today — a rise of roughly 25 per cent.

The scale of that figure deserves context. Education is already one of Britain’s largest export sectors, worth more than the automotive and food industries. The government estimates that international students contribute around £560 to the pocket of every UK citizen. For anyone who has ever had to justify the value of study-abroad programmes to a sceptical stakeholder, these are useful numbers to have to hand.

What has changed since the previous 2019 strategy is just as important as the target itself. The new strategy removes the numerical goal for onshore international student numbers — the old target of 600,000 was comfortably surpassed, with more than 700,000 students today, around 23 per cent of university enrolments. In its place, the focus shifts to growing the export of educational services, particularly through transnational education (TNE), an area where the UK leads the world with over 620,000 students enrolled in UK programmes across nearly 200 countries.

Why This Matters for Language Travel

For the language and study-holiday segment, one detail stands out. The strategy explicitly names English Language Training (ELT) as a priority growth area, alongside skills-based education and edtech. According to ICEF Monitor, the UK ELT sector generated around £996 million in direct revenue in 2024 — close to £2 billion when indirect impact is included.

Honesty matters when advising partners, so it is worth noting the fuller picture: the same ELT sector saw a dip in enrolments in the first half of 2025. Read in that light, the new strategy arrives not as a victory lap but as active government support for a segment seeking renewed momentum. That is a reassuring message. When the government of your primary destination market names your sector as a national priority, it speaks to the long-term stability of the destination.

The strategy also introduces a ministerially-led Education Sector Action Group, identifies priority partnership markets including India, Indonesia, Nigeria, Saudi Arabia and Vietnam, confirms a sixth year of the Turing Scheme, and sets out the UK’s return to Erasmus+ from 2027.

Ireland Reaches a Record High

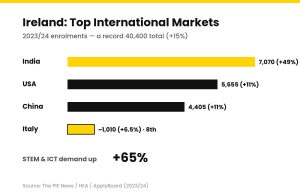

While the UK recalibrated its ambitions, Ireland was busy setting records. In 2023/24, the country recorded 40,400 international enrolments, crossing the 40,000 threshold for the first time and marking a 15 per cent increase on the previous year — a third consecutive year of growth.

The narrative behind the numbers is compelling. As traditional destinations such as Canada, Australia and the UK were unsettled by shifting immigration policies, Ireland positioned itself as a rising alternative, drawing students with lower living costs and strong post-study work opportunities.

The source markets tell their own story. India has become Ireland’s leading market with 7,070 students, a 49 per cent jump, overtaking the United States (5,655, up 11 per cent) and China (4,405, up 11 per cent). For our European audience, Italy sits in eighth place with around 1,010 students, up 6.5 per cent — and interest from EU students more broadly (German, Polish, Czech and Romanian among them) continues to climb. Part of the reason is Brexit: EU students now pay full international fees in the UK, making Ireland the more affordable English-speaking option. Demand for STEM and ICT courses has surged by 65 per cent.

A Market Building Around Quality

Ireland’s growth is not accidental. The national strategy Global Citizens 2030, Ireland’s Talent and Innovation Strategy launched in January 2024, targets a 10 per cent increase in international students, researchers and innovators by 2030. By January 2026, The PIE’s “Beyond the big four” overview confirmed that the Irish government regards international education as “very important,” in the words of the responsible minister.

The quality dimension is where Ireland’s story becomes especially relevant for partners. The country’s quality framework now has a formal name: TrustEd Ireland, a statutory quality mark managed by Quality and Qualifications Ireland (QQI). Crucially, it covers not only higher education institutions but also English language (ELT) providers. In January 2026, the first 28 TrustEd Ireland marks were awarded to higher education institutions. The mark is designed to protect international students and certify compliance with national standards.

For MLA, this is a value worth claiming. Operating in a market that is structuring itself around certified quality standards strengthens the confidence of agents and families alike.

The Common Thread: Growth With Quality

Step back, and a shared pattern emerges. Between January 2024 and January 2026, both of MLA’s core destinations received a strong strategic endorsement from their respective governments. And both endorsements share the same defining trait: growth paired with a focus on quality and sustainable recruitment — the Agent Quality Framework in the UK, TrustEd Ireland in Ireland.

This is the reassuring message for partners. These destinations are solid, institutionally supported, and increasingly oriented around quality. In a sector where trust and reliability determine which programmes families choose, that alignment is a genuine asset.

Two points of transparency keep the picture accurate. The UK’s £40 billion target covers total education exports — universities, TNE, ELT and edtech — rather than study holidays specifically, and the UK ELT sector did see a decline in the first half of 2025. Ireland’s 40,000-plus figure refers to higher education (HEA/ApplyBoard data), not exclusively the language-travel segment. Framed correctly, these caveats do not weaken the case; they reinforce a market maturing toward accountability and quality.

For partners planning their next intake, the takeaway is simple. The UK and Ireland are not merely popular choices — they are destinations their own governments are actively investing in, with quality frameworks that protect the students you send. That is a foundation worth building on.